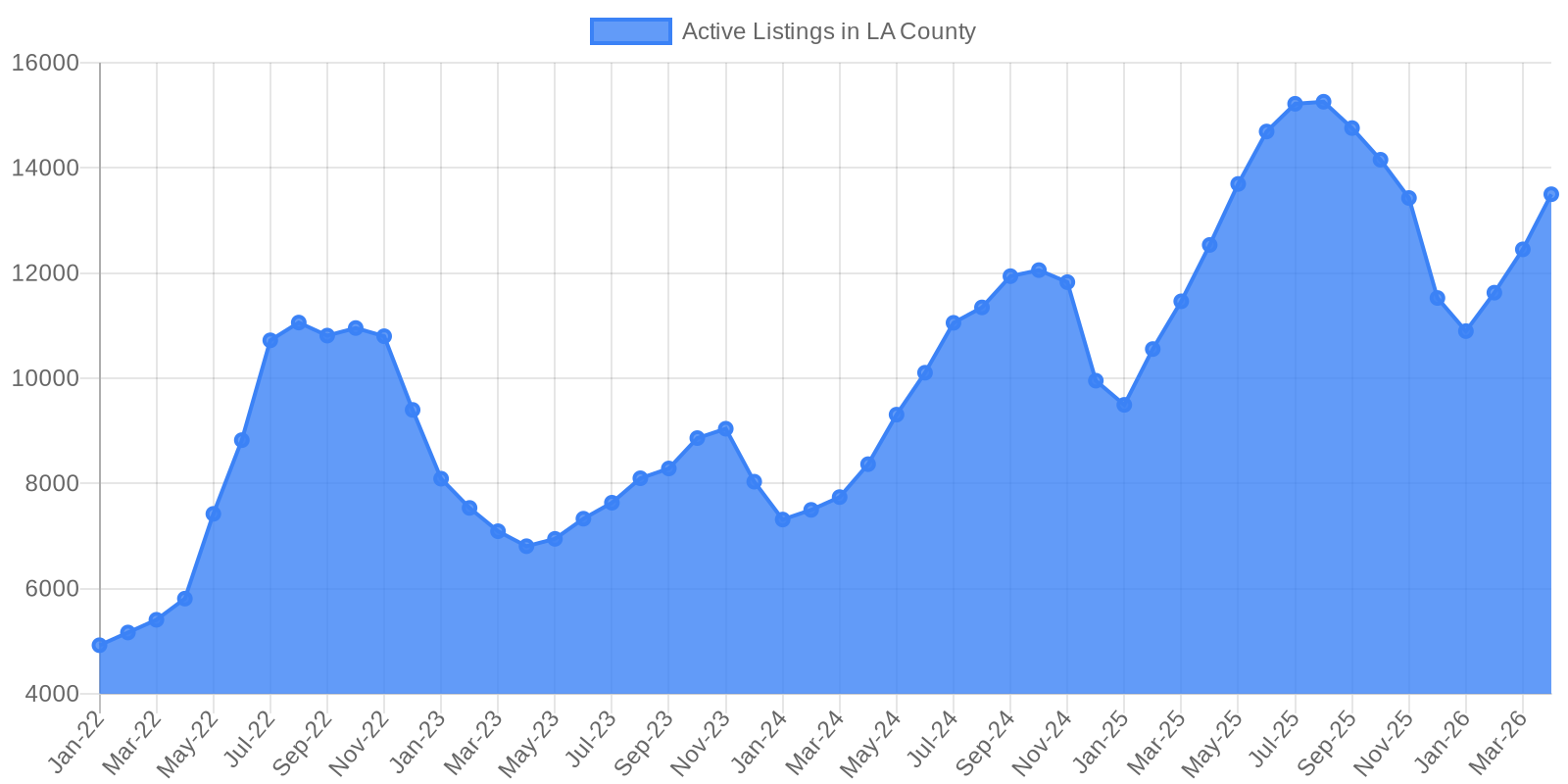

Los Angeles County's housing inventory has more than doubled over the past three years, climbing from just 4,923 active listings in January 2022 to 13,499 in April 2026—a 174% increase that marks the most dramatic shift in available homes since before the pandemic. This surge tells a story not of a housing crash, but of a market thawing after years of being frozen by historically low mortgage rates. And here's what makes this particularly significant: the inventory peaked at 15,258 listings in August 2025, the highest level since 2019, before settling into its current spring pattern around 13,500 homes. What we're watching unfold is the gradual breaking of what economists call the "lock-in effect"—and it's reshaping everything about how homes get bought and sold in America's second-largest city.

Active housing listings in Los Angeles County have more than doubled since early 2022, with inventory climbing from under 5,000 homes to over 13,000 by April 2026, marking the strongest supply growth since before the pandemic.

The data reveals three distinct phases in LA's inventory story. From January 2022 through August 2022, listings surged from under 5,000 to over 11,000 as rising interest rates began cooling the pandemic-era frenzy. Then came the contraction: inventory collapsed through 2023, bottoming out at just 6,806 listings in April 2023 as homeowners with sub-4% mortgages locked themselves into their properties. But the real story begins in 2024. Starting that spring, listings began climbing again—steadily, persistently—rising from 7,313 in January 2024 to 12,056 by October 2024. That upward march continued through 2025, with inventory growing 47% year-over-year in May 2025 and peaking above 15,000 homes that summer. Even accounting for seasonal dips each December and January, the trend is unmistakable: more sellers are returning to the market.

The numbers connect directly to what the LA Times reported in April 2026—that LA County recorded just 3,072 home sales in January 2026, the lowest monthly total in three years, and that homes spent a median 80 days on market in February, the longest stretch in five years. This disconnect between rising inventory and sluggish sales reflects a market where 630,000 more sellers than buyers exist nationwide, the largest gap on record since 2013. The catalyst for recent volatility was geopolitical: the Iran war that erupted in early 2026 spiked mortgage rates back to 6.5%, pulling cautious buyers off the sidelines. But even before that shock, the underlying dynamic was clear—inventory was climbing because the financial advantage of staying locked in was eroding. As real estate agents noted in the Times piece, new escrows increased up to 50% in recent weeks following the ceasefire, suggesting that recorded sales will soon catch up to the growing supply.

The lock-in effect is unwinding for structural reasons that go far beyond short-term rate fluctuations. A Bankrate survey found that 54% of U.S. homeowners wouldn't sell at any mortgage rate in 2025, yet that psychological barrier is cracking. By early 2026, more mortgage holders likely carry rates above 6% than below 3%, fundamentally changing the calculus. When millions of homeowners purchased or refinanced in 2022-2024 at higher rates, they eliminated their own payment advantage—making the next move less financially painful. Meanwhile, life doesn't pause: people get new jobs, grow families, downsize after retirement, or simply want different neighborhoods. These life-cycle pressures are now strong enough to overcome rate anxiety. Research from the Federal Housing Finance Agency shows each percentage point of lock-in reduces sale probability by 18%, but that effect weakens as the pool of ultra-low-rate holders shrinks and as financial stress, job changes, and demographic shifts force more hands. The data confirms it: inventory in LA County increased 28% in 2024 and another 12% in 2025, while for-sale inventory is now within 9% of pre-pandemic norms nationally.

Los Angeles isn't experiencing a housing crash—it's experiencing normalization. The inventory surge from 4,923 to 13,499 listings represents a market finding equilibrium after years of artificial constraint. Sellers are slowly accepting that waiting for 3% rates means waiting forever, while buyers who lock in today's 6-6.5% rates can always refinance later if conditions improve. What's emerging is a more balanced market where homes take longer to sell, price cuts are common, and buyers have actual negotiating power—a stark contrast to the bidding wars of 2020-2021. For anyone watching this market, the message is clear: the inventory drought is ending not with a sudden flood, but with a steady, structural thaw that will define LA real estate for years to come.