Los Angeles issued 5,394 building permits in April 2026, a sharp pullback from March's 5,831 permits that represents a 7.5% month-over-month decline. For construction contractors tracking project pipelines, this drop comes at a particularly sensitive moment—right after permit fees increased 5 to 7% in February 2026 and new Title 24 Energy Code requirements took effect January 1, 2026, adding stricter insulation and solar mandates. The April figure also sits 1.8% below last year's April 2025 count of 5,493 permits. While Los Angeles contractors have navigated plenty of regulatory changes over the years, this particular combination—higher fees, tougher code requirements, and declining permit volume—points to a more cautious market heading into the typically busy summer construction season.

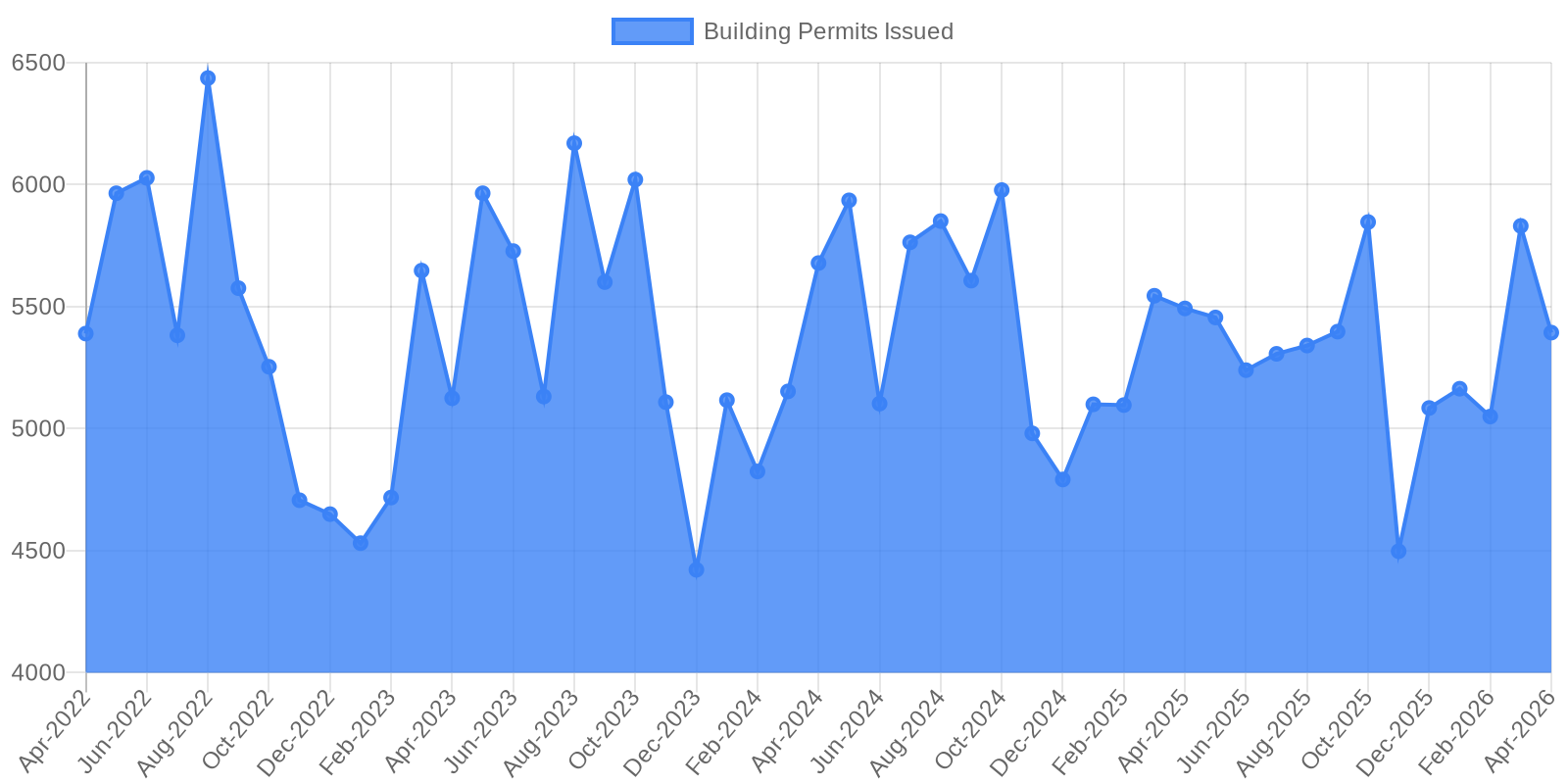

Monthly building permit issuance in Los Angeles from April 2022 through April 2026 shows consistent seasonal patterns with November lows and August peaks, though overall volumes have stabilized in a lower 5,300-5,500 range for spring months compared to 6,000-plus peaks in 2022-2023.

The monthly data reveals clear seasonal patterns that contractors should account for when planning capacity and cash flow. November consistently marks the year's low point: permits dropped to 4,707 in November 2022, 5,109 in November 2023, 4,981 in November 2024, and 4,498 in November 2025. August typically delivers the year's peak, with 6,437 permits in August 2022, 6,170 in August 2023, and 5,851 in August 2024. March often shows a spring rebound—March 2023 hit 5,648 permits, March 2024 reached 5,153, March 2025 climbed to 5,545, and March 2026 jumped to 5,831. April's 5,394 permits breaks that upward momentum. Year-over-year comparisons also show the market flattening out: April 2022 logged 5,390 permits, April 2023 saw 5,125, April 2024 recorded 5,679, April 2025 hit 5,493, and April 2026 came in at 5,394. The data suggests the Los Angeles construction market has stabilized in a lower range than the 6,000-plus peaks seen in 2022 and 2023, settling into a steady 5,300-5,500 permit range for spring months.

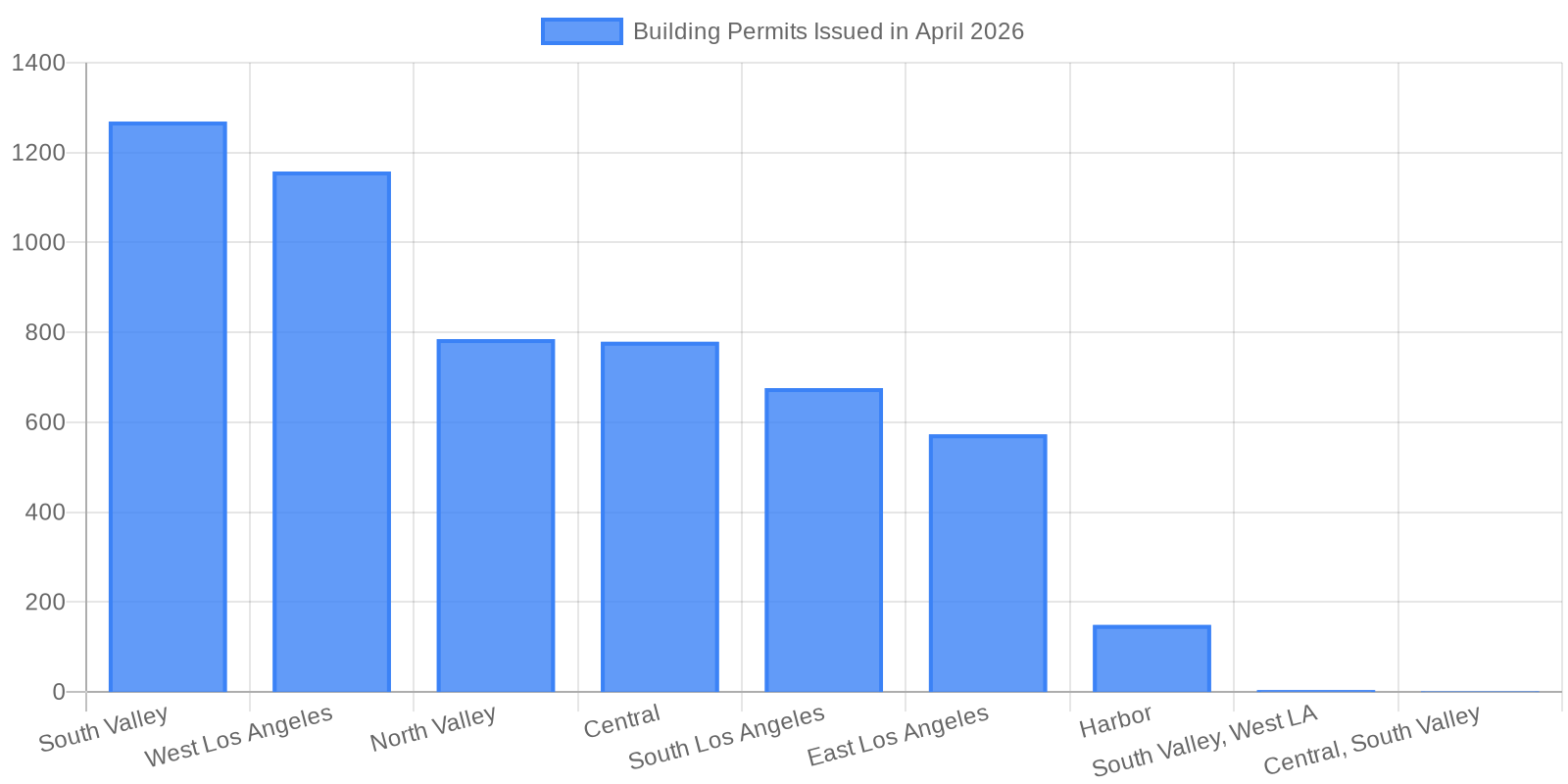

South Valley and West Los Angeles accounted for nearly half of all April 2026 permits, with 1,269 and 1,158 permits respectively—together representing 45% of the city's total activity. North Valley added 785 permits and Central Los Angeles contributed 779, while South Los Angeles, East Los Angeles, and Harbor regions lagged with 676, 573, and 149 permits respectively. This geographic concentration creates a clear strategy divide for contractors: firms focused on South Valley and West LA have significantly more near-term opportunities, while those serving Harbor or East LA face tougher volume headwinds. The regional breakdown also reflects broader housing patterns—South Valley and West LA's dominance aligns with where affordable housing funding and ADU growth are positives, but Los Angeles apartment construction remains weak.

South Valley and West Los Angeles dominated April 2026 permit activity with 1,269 and 1,158 permits respectively, accounting for 45% of citywide issuance, while Harbor region recorded just 149 permits.

The permit slowdown reflects broader pressures on California construction. Single family residential construction starts during the six-month phase ending February 2026 were down 11% from the same phase one year earlier, while multi-family construction starts were up 74.5% from a year earlier. Nationally, privately-owned housing units authorized by building permits in April were at a seasonally adjusted annual rate of 1,442,000, which is 5.8 percent above the revised March rate of 1,363,000, but is 0.2 percent below the April 2025 rate. Los Angeles contractors should note that the local April decline mirrors this national near-flat trajectory. Meanwhile, LADBS fees were last updated in February 2026, with a 5 to 7% increase, and the 2025 Title 24 Energy Code introduces stricter insulation requirements, expanded solar PV mandates, and new battery storage requirements—all adding upfront costs that may be discouraging marginal projects. For 2026, we will see a much-diminished residential development environment as economic uncertainty weighs on investor confidence.

For Los Angeles contractors, April's numbers suggest a market in wait-and-see mode rather than crisis. Seasonal patterns remain intact—expect permit activity to climb through summer toward an August peak—but the overall baseline has shifted lower compared to 2022-2023 levels. The regional concentration in South Valley and West LA means workload allocation matters more than ever: contractors with diversified geographic reach can pivot toward higher-volume areas, while those locked into slower regions face tougher margin pressures. The March-to-April drop also serves as a reminder that single-month spikes don't necessarily signal sustained momentum. With permit timelines ranging from weeks to months depending on project scope and review backlog, contractors should build project pipelines with realistic lead times and avoid overcommitting capacity based on one strong month. The permit data doesn't point to collapse, but it clearly signals a market where careful planning and cost discipline will separate profitable firms from struggling ones through the rest of 2026.