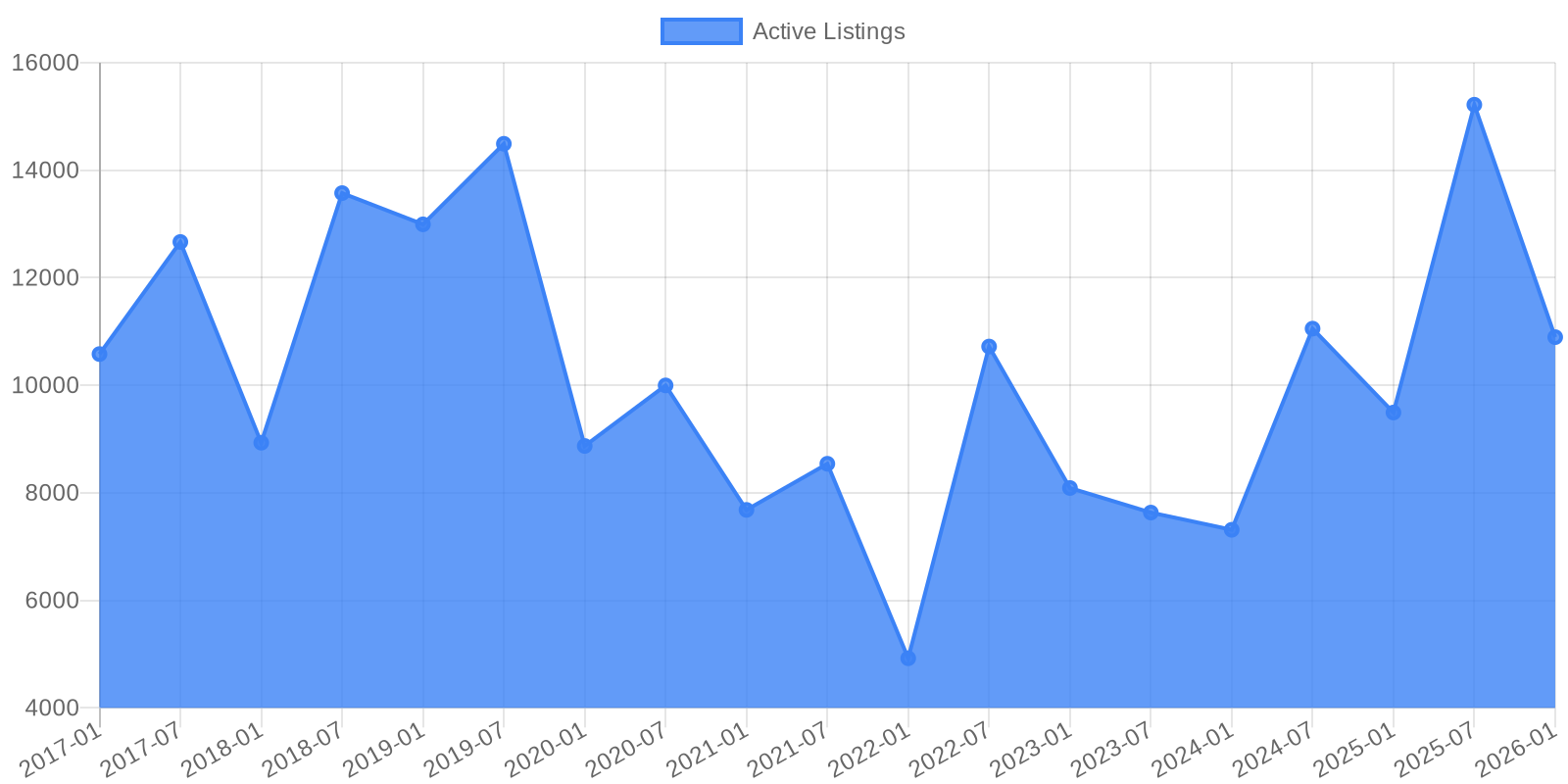

Los Angeles County's housing market just crossed a threshold most buyers thought they'd never see again. In April 2026, active listings reached 13,499 homes—the highest level since mid-2019, when the market last operated under something resembling normal conditions. This isn't a crash. It's a normalization. And it signals the end of the pandemic-era seller's market that left buyers scrambling for scraps. The data shows a clear, unmistakable trend: inventory is surging, and the power dynamic between buyers and sellers is fundamentally rebalancing. That's not speculation—it's what happens when supply grows faster than demand can absorb it.

Los Angeles County active housing inventory (2017-2026) shows a dramatic collapse to a historic low of 4,923 in January 2022, followed by a sustained recovery to April 2026's seven-year high of 13,499 homes—signaling a fundamental shift from seller's to balanced market conditions.

The chart tells a story in three acts. From 2017 through early 2019, Los Angeles maintained a relatively stable inventory between 10,000 and 15,600 homes for sale, with predictable seasonal swings. Then came the pandemic shock: listings collapsed to a historic low of just 4,923 in January 2022 as buyer fear of missing out drove a buying frenzy. That moment—less than 5,000 homes available in a county of 10 million people—defined the market madness of 2021-2022. But starting in mid-2022, the trend reversed. Inventory began climbing steadily, and by 2025 it accelerated sharply. April 2026's count of 13,499 represents a 160% increase from the 2022 low and sits just 8% below the April 2019 level of 14,692. The recovery isn't complete, but it's unmistakable.

The control data from Realtor.com confirms what the inventory surge predicts: the market is cooling in real time. As of April 2026, active listings in Los Angeles stood at 11,484, up 4.28% year-over-year, while the median listing price dropped 7.85% to $1.15 million. Homes are sitting on the market longer—47 days in April, up 9.30% from the prior year—giving buyers time to evaluate and negotiate rather than panic-bid. This aligns with a broader pattern: inventory in Los Angeles increased 28% in 2024 and another 12% in 2025, with analysts expecting continued growth in 2026. Meanwhile, year-over-year home value growth slowed to just 1.9% in May 2025, down from 7.4% in 2024—barely above inflation. The data points all move in the same direction: more supply, softer prices, longer selling times.

Why does rising inventory matter so much? Because it changes everything about how the market works. When inventory surges but buyer demand doesn't keep pace, sellers lose pricing power and buyers gain leverage. A balanced market typically requires 5-7 months of supply; Los Angeles now sits at roughly 4.6 months, up from the sub-2-month levels that defined the pandemic frenzy. This shift is playing out in price cuts: nationally, price reductions hit 24.6% of all listings in May 2025, the highest May rate on record. In Los Angeles specifically, the sale-to-list ratio dropped to 97.91% in February 2026, meaning homes are selling below asking price—a stark reversal from 2021 when bidding wars pushed prices 10-20% over list. The mechanics are straightforward: when inventory rises, buyers wait for better deals, sellers reduce prices to attract offers, and the cycle continues until prices stabilize. That process is well underway in Los Angeles.

The inventory surge isn't likely to reverse anytime soon. Sales volume in LA County is down 6% year-to-date through February 2026, meaning homes are piling up faster than they're selling. New construction remains limited, but that constraint now works differently: instead of propping up prices, limited supply just means the existing inventory takes longer to clear. Many homeowners remain locked into low pandemic-era mortgage rates, creating what analysts call the "golden handcuff" effect that keeps some would-be sellers sidelined. But enough are listing—whether driven by job changes, family needs, or financial pressure—to keep inventory rising. For buyers who spent years on the sidelines, this is the opening they've been waiting for. Not a collapse, but a chance to negotiate, evaluate, and buy without panic. The frenzy is over. The question now is how long the adjustment takes to reach a true equilibrium.